Notes

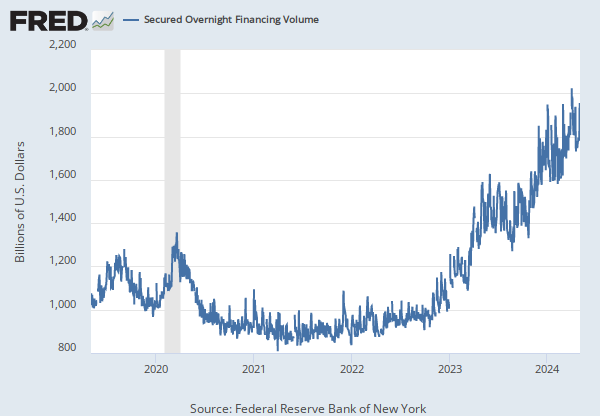

Source: Federal Reserve Bank of New York

Release: Overnight Bank Funding Rate Data

Units:

Frequency:

Notes:

The overnight bank funding rate is calculated using federal funds transactions and certain Eurodollar transactions. The federal funds market consists of domestic unsecured borrowings in U.S. dollars by depository institutions from other depository institutions and certain other entities, primarily government-sponsored enterprises, while the Eurodollar market consists of unsecured U.S. dollar deposits held at banks or bank branches outside of the United States. U.S.-based banks can also take Eurodollar deposits domestically through international banking facilities (IBFs). The overnight bank funding rate (OBFR) is calculated as a volume-weighted median of overnight federal funds transactions and Eurodollar transactions reported in the FR 2420 Report of Selected Money Market Rates.

Volume-weighted median is the rate associated with transactions at the 50th percentile of transaction volume. Specifically, the volume-weighted median rate is calculated by ordering the transactions from lowest to highest rate, taking the cumulative sum of volumes of these transactions, and identifying the rate associated with the trades at the 50th percentile of dollar volume. The published rates are the volume-weighted median transacted rate, rounded to the nearest basis point.

For more information, see https://www.newyorkfed.org/markets/obfrinfo

Suggested Citation:

Federal Reserve Bank of New York, Overnight Bank Funding Rate [OBFR], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/OBFR, .

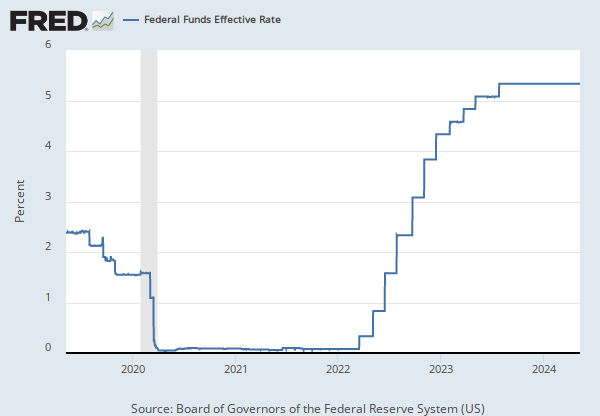

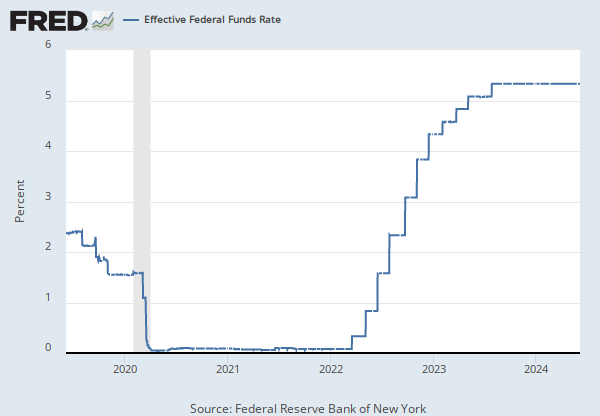

Source: Federal Reserve Bank of New York

Release: Federal Funds Data

Units:

Frequency:

Notes:

For additional historical federal funds rate data, please see Daily Federal Funds Rate from 1928-1954.

The federal funds market consists of domestic unsecured borrowings in U.S. dollars by depository institutions from other depository institutions and certain other entities, primarily government-sponsored enterprises.

The effective federal funds rate (EFFR) is calculated as a volume-weighted median of overnight federal funds transactions reported in the FR 2420 Report of Selected Money Market Rates.

For more information, visit the Federal Reserve Bank of New York.

Suggested Citation:

Federal Reserve Bank of New York, Effective Federal Funds Rate [EFFR], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/EFFR, .

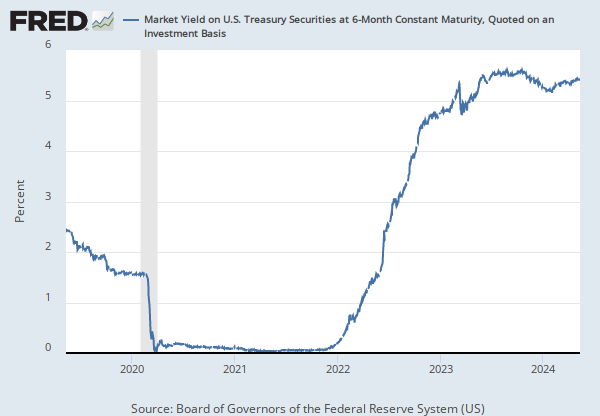

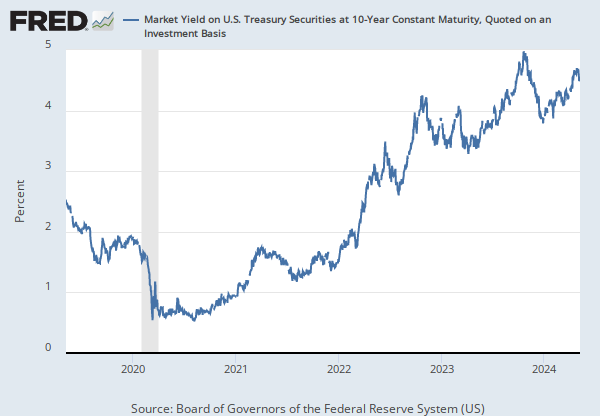

Source: Board of Governors of the Federal Reserve System (US)

Release: H.15 Selected Interest Rates

Units:

Frequency:

Notes:

For further information regarding treasury constant maturity data, please refer to the H.15 Statistical Release notes and the Treasury Yield Curve Methodology.

For questions on the data, please contact the data source. For questions on FRED functionality, please contact us here.

Suggested Citation:

Board of Governors of the Federal Reserve System (US), Market Yield on U.S. Treasury Securities at 1-Month Constant Maturity, Quoted on an Investment Basis [DGS1MO], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/DGS1MO, .

Release Tables

H.15 Selected Interest Rates

Related Data and Content

Data Suggestions Based On Your Search

Content Suggestions

Other Formats

Related Categories

FRB Rates - discount, fed funds, primary credit

Interest Rates

Money, Banking, & Finance

Treasury Constant Maturity

Releases

More

Series from Overnight Bank Funding Rate Data

More

Series from Federal Funds Data

More

Series from H.15 Selected Interest Rates

Tags

International Banking Facilities

Overnight

New York Fed

Percentile

Daily

Banks

Depository Institutions

Rate

Copyrighted: Citation Required

Nation

United States of America

Not Seasonally Adjusted

Federal

1-Month

Bills

H.15 Selected Interest Rates

Maturity

Treasury

Interest Rate

Interest

Board of Governors

Public Domain: Citation Requested