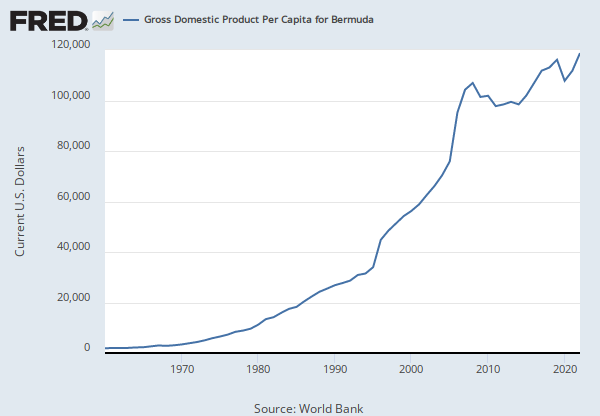

Observations

2021: 18.72809 | Z-score, Not Seasonally Adjusted | Annual

Updated: May 7, 2024 3:30 PM CDT

Next Release Date: Not Available

Observations

2021:

18.72809

Updated:

May 7, 2024

3:30 PM CDT

Next Release Date:

Not Available

| 2021: | 18.72809 | |

| 2020: | 20.18716 | |

| 2019: | 22.26934 | |

| 2018: | 26.09518 | |

| 2017: | 23.82868 | |

| View All | ||

Units:

Z-score,

Not Seasonally Adjusted

Frequency:

Annual

Fullscreen