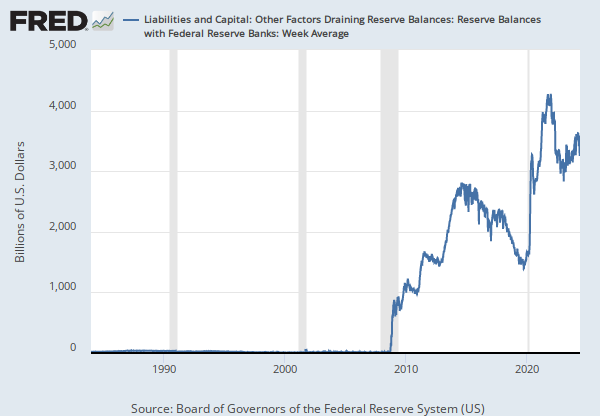

Notes

Source: Board of Governors of the Federal Reserve System (US)

Release: H.4.1 Factors Affecting Reserve Balances

Units:

Frequency:

Notes:

For questions on the data, please contact the data source. For questions on FRED functionality, please contact us here.

Suggested Citation:

Board of Governors of the Federal Reserve System (US), Assets: Other: Repurchase Agreements: Wednesday Level [WORAL], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/WORAL, .

Source: Board of Governors of the Federal Reserve System (US)

Release: H.4.1 Factors Affecting Reserve Balances

Units:

Frequency:

Notes:

For questions on the data, please contact the data source. For questions on FRED functionality, please contact us here.

Suggested Citation:

Board of Governors of the Federal Reserve System (US), Liabilities and Capital: Liabilities: Reverse Repurchase Agreements: Wednesday Level [WLRRAL], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/WLRRAL, .

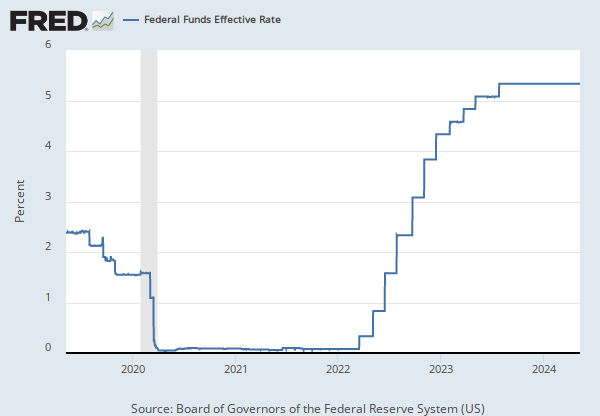

Source: Federal Reserve Bank of New York

Release: Federal Funds Data

Units:

Frequency:

Notes:

For additional historical federal funds rate data, please see Daily Federal Funds Rate from 1928-1954.

The federal funds market consists of domestic unsecured borrowings in U.S. dollars by depository institutions from other depository institutions and certain other entities, primarily government-sponsored enterprises.

The effective federal funds rate (EFFR) is calculated as a volume-weighted median of overnight federal funds transactions reported in the FR 2420 Report of Selected Money Market Rates.

For more information, visit the Federal Reserve Bank of New York.

Suggested Citation:

Federal Reserve Bank of New York, Effective Federal Funds Rate [EFFR], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/EFFR, .

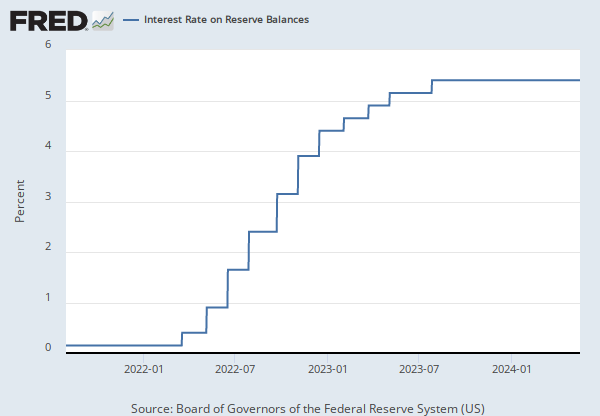

Release Tables

H.4.1 Factors Affecting Reserve Balances

- Table 1. Factors Affecting Reserve Balances of Depository Institutions: Wednesday Level

- Table 2. Maturity Distribution of Securities, Loans, and Selected Other Assets and Liabilities

- Table 5. Consolidated Statement of Condition of All Federal Reserve Banks

- Table 6. Statement of Condition of Each Federal Reserve Bank

Related Data and Content

Data Suggestions Based On Your Search

Content Suggestions

Related Categories

Factors Affecting Reserve Balances

Monetary Data

Money, Banking, & Finance

FRB Rates - discount, fed funds, primary credit

Interest Rates