Notes

Source: Federal Reserve Bank of St. Louis

Release: Interest Rate Spreads

Units:

Frequency:

Notes:

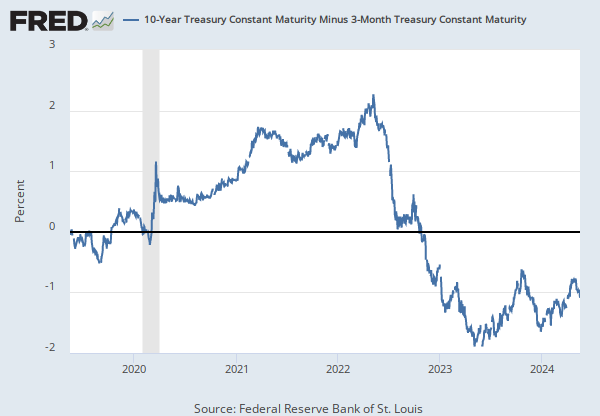

Series is calculated as the spread between 10-Year Treasury Constant Maturity (BC_10YEAR) and Effective Federal Funds Rate (https://fred.stlouisfed.org/series/EFFR).

Starting with the update on June 21, 2019, the Treasury bond data used in calculating interest rate spreads is obtained directly from the U.S. Treasury Department.

Suggested Citation:

Federal Reserve Bank of St. Louis, 10-Year Treasury Constant Maturity Minus Federal Funds Rate [T10YFF], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/T10YFF, .

Source: Federal Reserve Bank of St. Louis

Release: Interest Rate Spreads

Units:

Frequency:

Notes:

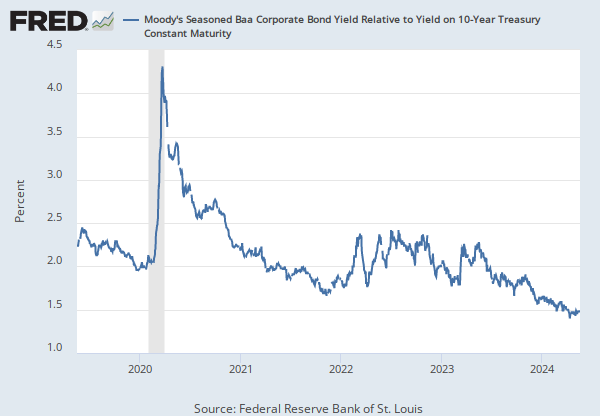

Series is calculated as the spread between 3-Month LIBOR based on US dollars (USD3MTD156N) and 3-Month Treasury Bill (DTB3).

Starting with the update on June 21, 2019, the Treasury bond data used in calculating interest rate spreads is obtained directly from the U.S. Treasury Department.

The 3-Month LIBOR based on US Dollars has been removed from FRED as of January 31, 2022, so this calculated series has been discontinued and will no longer be updated. Users interested in calculating a similar credit risk can use the Secured Overnight Financing Rate (SOFR), which has been identified as the rate that represents best practice for use in certain new U.S. Dollar derivatives and other financial contracts. For more details, see the article Transition from LIBOR from the Alternative Reference Rates Committee (AARC).

Suggested Citation:

Federal Reserve Bank of St. Louis, TED Spread (DISCONTINUED) [TEDRATE], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/TEDRATE, .