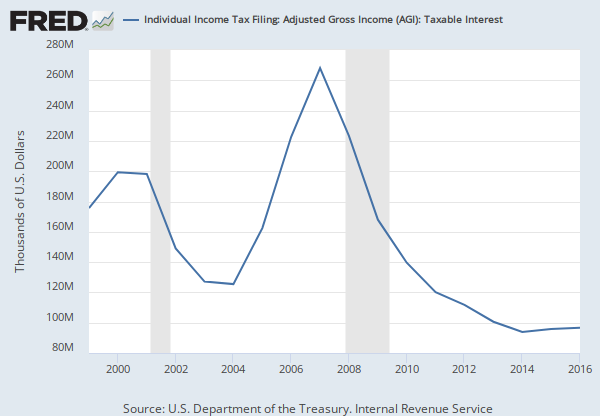

Observations

2016: 202,033,794 | Thousands of U.S. Dollars, Not Seasonally Adjusted | Annual

Updated: Dec 19, 2018 1:31 PM CST

Next Release Date: Not Available

Observations

2016:

202,033,794

Updated:

Dec 19, 2018

1:31 PM CST

Next Release Date:

Not Available

| 2016: | 202,033,794 | |

| 2015: | 203,187,788 | |

| 2014: | 192,447,711 | |

| 2013: | 158,069,115 | |

| 2012: | 204,401,524 | |

| View All | ||

Units:

Thousands of U.S. Dollars,

Not Seasonally Adjusted

Frequency:

Annual

Fullscreen