Notes

Source: Federal Reserve Bank of St. Louis

Release: Interest Rate Spreads

Units:

Frequency:

Notes:

Starting with the update on June 21, 2019, the Treasury bond data used in calculating interest rate spreads is obtained directly from the U.S. Treasury Department.

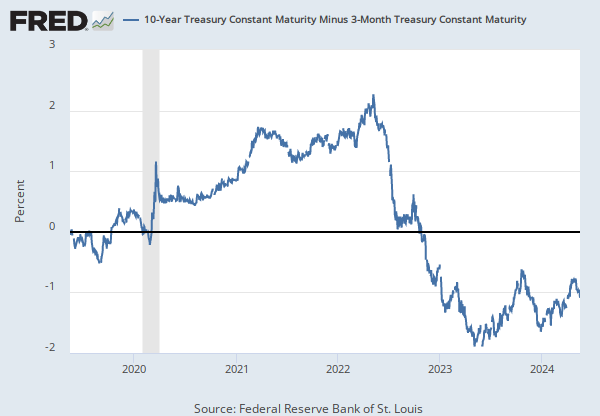

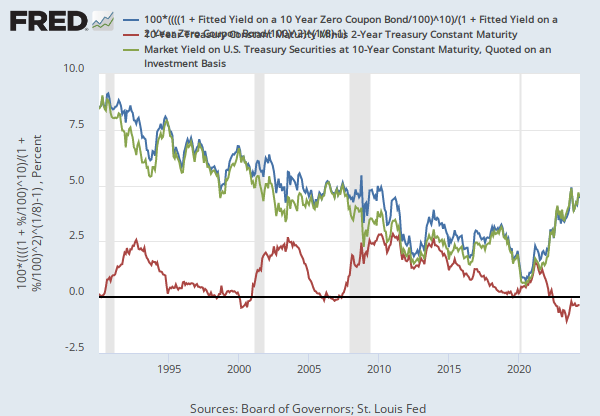

Series is calculated as the spread between 10-Year Treasury Constant Maturity (BC_10YEAR) and 2-Year Treasury Constant Maturity (BC_2YEAR). Both underlying series are published at the U.S. Treasury Department.

Suggested Citation:

Federal Reserve Bank of St. Louis, 10-Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity [T10Y2Y], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/T10Y2Y, .

Source: S&P Dow Jones Indices LLC

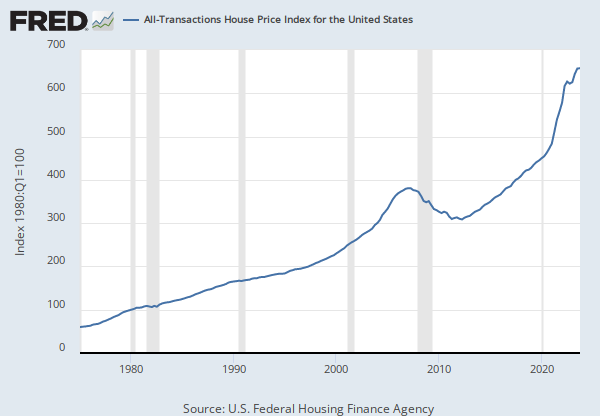

Release: S&P Cotality Case-Shiller Home Price Indices

Units:

Frequency:

Notes:

For more information regarding the index, please visit Standard & Poor's. There is more information about home price sales pairs in the Methodology section. Copyright, 2016, Standard & Poor's Financial Services LLC. Reprinted with permission.

Suggested Citation:

S&P Dow Jones Indices LLC, S&P Cotality Case-Shiller U.S. National Home Price Index [CSUSHPISA], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/CSUSHPISA, .

Release Tables

S&P Cotality Case-Shiller Home Price Indices

Related Data and Content

Data Suggestions Based On Your Search

Content Suggestions

Other Formats

10-Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity

Monthly, Not Seasonally AdjustedS&P Cotality Case-Shiller U.S. National Home Price Index

Monthly, Not Seasonally AdjustedRelated Categories

Releases

More

Series from Interest Rate Spreads

More

Series from S&P Cotality Case-Shiller Home Price Indices

Tags

2-Year

Yield Curve

Spread

10-Year

Maturity

Treasury

Interest Rate

Interest

Daily

St. Louis Fed

Rate

Copyrighted: Citation Required

Nation

United States of America

Not Seasonally Adjusted

S&P Cotality Case-Shiller Home Price Indices

S&P Dow Jones Indices LLC

House Price Index

Copyrighted: Pre-Approval Required

Housing

Price Index

Indexes

Price

Seasonally Adjusted

Monthly