Notes

Source: Board of Governors of the Federal Reserve System (US)

Release: H.15 Selected Interest Rates

Units:

Frequency:

Notes:

For further information regarding treasury constant maturity data, please refer to the H.15 Statistical Release notes and Treasury Yield Curve Methodology.

For questions on the data, please contact the data source. For questions on FRED functionality, please contact us here.

Suggested Citation:

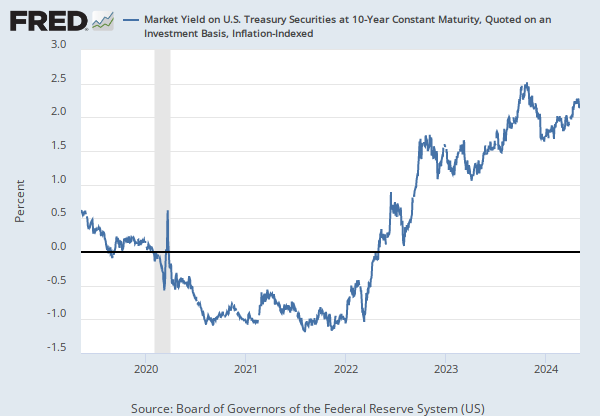

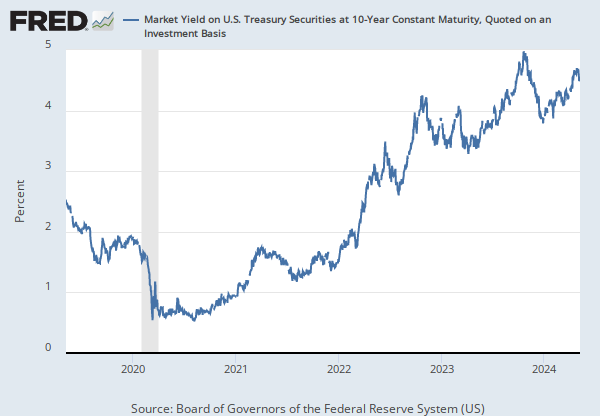

Board of Governors of the Federal Reserve System (US), Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity, Quoted on an Investment Basis [DGS10], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/DGS10, .

Source: Board of Governors of the Federal Reserve System (US)

Release: H.15 Selected Interest Rates

Units:

Frequency:

Notes:

For further information regarding treasury constant maturity data, please refer to the H.15 Statistical Release notes and the Treasury Yield Curve Methodology.

For questions on the data, please contact the data source. For questions on FRED functionality, please contact us here.

Suggested Citation:

Board of Governors of the Federal Reserve System (US), Market Yield on U.S. Treasury Securities at 2-Year Constant Maturity, Quoted on an Investment Basis [DGS2], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/DGS2, .

Source: Federal Reserve Bank of St. Louis

Release: Interest Rate Spreads

Units:

Frequency:

Notes:

Series is calculated as the spread between 3-Month LIBOR based on US dollars (USD3MTD156N) and 3-Month Treasury Bill (DTB3).

Starting with the update on June 21, 2019, the Treasury bond data used in calculating interest rate spreads is obtained directly from the U.S. Treasury Department.

The 3-Month LIBOR based on US Dollars has been removed from FRED as of January 31, 2022, so this calculated series has been discontinued and will no longer be updated. Users interested in calculating a similar credit risk can use the Secured Overnight Financing Rate (SOFR), which has been identified as the rate that represents best practice for use in certain new U.S. Dollar derivatives and other financial contracts. For more details, see the article Transition from LIBOR from the Alternative Reference Rates Committee (AARC).

Suggested Citation:

Federal Reserve Bank of St. Louis, TED Spread (DISCONTINUED) [TEDRATE], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/TEDRATE, .

Source: Federal Reserve Bank of St. Louis

Release: St. Louis Fed Financial Stress Index

Units:

Frequency:

Notes:

The methodology for the St. Louis Fed's Financial Stress Index was revised and this series is discontinued. The new version, STLFSI3, can be found here.

The STLFSI2 measures the degree of financial stress in the markets and is constructed from 18 weekly data series, all of which are weekly averages of daily data series: seven interest rates, six yield spreads, and five other indicators. Each of these variables captures some aspect of financial stress. Accordingly, as the level of financial stress in the economy changes, the data series are likely to move together.

How to Interpret the Index:

The average value of the index, which begins in late 1993, is designed to be zero. Thus, zero is viewed as representing normal financial market conditions. Values below zero suggest below-average financial market stress, while values above zero suggest above-average financial market stress.

More information:

The STLFSI2 is a revision of the original STLFSI. For additional information on the STLFSI2 and its construction, see “The St. Louis Fed’s Financial Stress Index, Version 2.0”.

Suggested Citation:

Federal Reserve Bank of St. Louis, St. Louis Fed Financial Stress Index (DISCONTINUED) [STLFSI2], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/STLFSI2, .

Release Tables

H.15 Selected Interest Rates

Related Data and Content

Data Suggestions Based On Your Search

Content Suggestions

Other Formats

Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity, Quoted on an Investment Basis

Annual, Not Seasonally Adjusted Monthly, Not Seasonally Adjusted Weekly, Not Seasonally AdjustedMarket Yield on U.S. Treasury Securities at 2-Year Constant Maturity, Quoted on an Investment Basis

Annual, Not Seasonally Adjusted Monthly, Not Seasonally Adjusted Weekly, Not Seasonally AdjustedSt. Louis Fed Financial Stress Index (DISCONTINUED)

Weekly, Not Seasonally Adjusted Weekly, Not Seasonally AdjustedRelated Categories

Treasury Constant Maturity

Interest Rates

Money, Banking, & Finance

Interest Rate Spreads

Financial Activity Measures

Financial Indicators

Releases

More

Series from H.15 Selected Interest Rates

More

Series from Interest Rate Spreads

More

Series from St. Louis Fed Financial Stress Index

Tags

10-Year

H.15 Selected Interest Rates

Maturity

Treasury

Interest Rate

Interest

Daily

Board of Governors

Rate

Nation

Public Domain: Citation Requested

United States of America

Not Seasonally Adjusted

2-Year

London Interbank Offered Rate

Yield Curve

Spread

Bills

3-Month

Discontinued

St. Louis Fed

Copyrighted: Citation Required

St. Louis Financial Stress Index

Financial Stress Index

Financial

Weekly

Indexes