Notes

Source: Federal Reserve Bank of St. Louis

Release: Interest Rate Spreads

Units:

Frequency:

Notes:

Series is calculated as the spread between 10-Year Treasury Constant Maturity (BC_10YEAR) and 3-Month Treasury Constant Maturity (BC_3MONTH).

Starting with the update on June 21, 2019, the Treasury bond data used in calculating interest rate spreads is obtained directly from the U.S. Treasury Department.

Suggested Citation:

Federal Reserve Bank of St. Louis, 10-Year Treasury Constant Maturity Minus 3-Month Treasury Constant Maturity [T10Y3M], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/T10Y3M, .

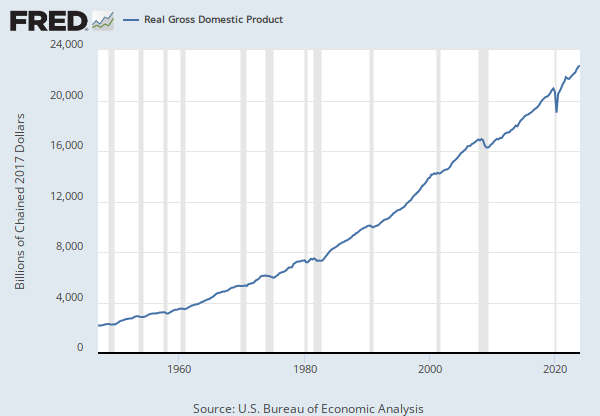

Source: U.S. Bureau of Economic Analysis

Release: Gross Domestic Product

Units:

Frequency:

Notes:

BEA Account Code: A191RC

Gross domestic product (GDP), the featured measure of U.S. output, is the market value of the goods and services produced by labor and property located in the United States.For more information, see the Guide to the National Income and Product Accounts of the United States (NIPA) and the Bureau of Economic Analysis.

Suggested Citation:

U.S. Bureau of Economic Analysis, Gross Domestic Product [GDP], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/GDP, .

Source: American Financial Exchange

Release: Historical Overnight AMERIBOR Unsecured Interest Rate

Units:

Frequency:

Notes:

AMERIBOR® (American Interbank Offered Rate) is a benchmark interest rate based on overnight unsecured loans transacted on the American Financial Exchange (AFX). AMERIBOR® is calculated as the transaction volume weighted average interest rate of the daily transactions in the AMERIBOR® overnight unsecured loan market on the AFX. The arbitrage free AMERIBOR® Term Structure of Interest Rates is derived from the Overnight Unsecured AMERIBOR® Interest Rate (AMERIBOR) and the implied AMERIBOR® forward rates from the AMERIBOR® futures prices. More details about AMERIBOR® methodology can be found on the source's website, under the Resources section.

AMERIBOR® is a registered trademark of the American Financial Exchange (AFX). © Copyright, American Financial Exchange (AFX). All Rights Reserved.

Suggested Citation:

American Financial Exchange, 2-Year AMERIBOR Term Structure of Interest Rates (DISCONTINUED) [AMBOR2Y], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/AMBOR2Y, .

Source: Board of Governors of the Federal Reserve System (US)

Release: H.15 Selected Interest Rates

Units:

Frequency:

Notes:

For further information regarding treasury constant maturity data, please refer to the H.15 Statistical Release notes and the Treasury Yield Curve Methodology.

For questions on the data, please contact the data source. For questions on FRED functionality, please contact us here.

Suggested Citation:

Board of Governors of the Federal Reserve System (US), Market Yield on U.S. Treasury Securities at 2-Year Constant Maturity, Quoted on an Investment Basis [DGS2], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/DGS2, .

Release Tables

Gross Domestic Product

- Table 1.1.5. Gross Domestic Product: Quarterly

- Table 1.2.5. Gross Domestic Product by Major Type of Product: Quarterly

- Table 1.3.5. Gross Value Added by Sector: Quarterly

- Table 1.4.5. Relation of Gross Domestic Product, Gross Domestic Purchases, and Final Sales to Domestic Purchasers: Quarterly

- Table 1.5.5. Gross Domestic Product, Expanded Detail: Quarterly

- Table 1.7.5. Relation of Gross Domestic Product, Gross National Product, Net National Product, National Income, and Personal Income: Quarterly

- Table 1.17.5. Gross Domestic Product, Gross Domestic Income, and Other Major NIPA Aggregates: Quarterly

H.15 Selected Interest Rates

Historical Overnight AMERIBOR Unsecured Interest Rate

Related Data and Content

Data Suggestions Based On Your Search

Content Suggestions

Other Formats

10-Year Treasury Constant Maturity Minus 3-Month Treasury Constant Maturity

Monthly, Not Seasonally AdjustedGross Domestic Product

Annual, Not Seasonally Adjusted Annual, Not Seasonally Adjusted Index 2017=100, Quarterly, Not Seasonally Adjusted Millions of Dollars, Quarterly, Not Seasonally Adjusted Percent Change from Preceding Period, Annual, Not Seasonally Adjusted Percent Change from Preceding Period, Quarterly, Seasonally Adjusted Annual RateMarket Yield on U.S. Treasury Securities at 2-Year Constant Maturity, Quoted on an Investment Basis

Annual, Not Seasonally Adjusted Monthly, Not Seasonally Adjusted Weekly, Not Seasonally AdjustedRelated Categories

Interest Rate Spreads

Interest Rates

Money, Banking, & Finance

GDP/GNP

National Income & Product Accounts

National Accounts

AMERIBOR Benchmark Rates

Treasury Constant Maturity

Releases

More

Series from Interest Rate Spreads

More

Series from Gross Domestic Product

More

Series from Historical Overnight AMERIBOR Unsecured Interest Rate

More

Series from H.15 Selected Interest Rates

Tags

Yield Curve

Spread

3-Month

10-Year

Maturity

Treasury

Interest Rate

Interest

St. Louis Fed

Daily

Rate

Copyrighted: Citation Required

Nation

United States of America

Not Seasonally Adjusted

National Income and Product Accounts

Bureau of Economic Analysis

Gross Domestic Product

Quarterly

Seasonally Adjusted

Public Domain: Citation Requested

American Interbank Offered Rate

American Financial Exchange

2-Year

Discontinued

H.15 Selected Interest Rates

Board of Governors