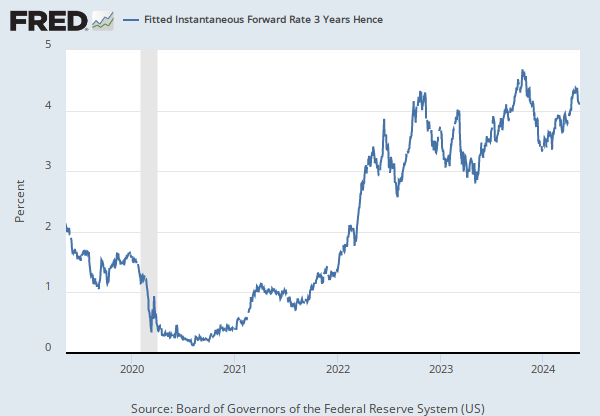

Observations

2026-07-17: 4.6896 | Percent, Not Seasonally Adjusted | Daily

Updated: Jul 21, 2026 2:04 PM CDT

Next Release Date: Not Available

Observations

2026-07-17:

4.6896

Updated:

Jul 21, 2026

2:04 PM CDT

Next Release Date:

Not Available

| 2026-07-17: | 4.6896 | |

| 2026-07-16: | 4.6930 | |

| 2026-07-15: | 4.6743 | |

| 2026-07-14: | 4.7032 | |

| 2026-07-13: | 4.7255 | |

| View All | ||

Units:

Percent,

Not Seasonally Adjusted

Frequency:

Daily

Fullscreen